Once simple work machines, today’s so-called Yellow Fleet has become the backbone of modern railway infrastructure. These multi-functional vehicles not only build new lines but also maintain and upgrade heavily used networks, making them indispensable for a reliable and efficient rail system.

The latest SCI market study, 'Yellow Fleet – Global Market & Trends 2025', describes how rapid technological progress has turned these machines into all-rounders. Where once multiple vehicles had to be coordinated, a single modern unit can now perform automated and digitalised processes in construction, electrification, and maintenance. Tamping machines, renewal trains, and overhead line construction vehicles are key indicators of the health of a country’s rail infrastructure.

With 7,000 vehicles out of 27,000 worldwide, Europe is the largest market, led by Germany, France and Italy. Asia follows with 4,900 units, driven by large-scale projects in China and India. The United States counts more than 4,000 vehicles, primarily used on freight lines, while Russia dominates the sizeable but ageing fleets of the CIS states. Smaller but growing markets are found in Latin America, Africa and the Middle East, where targeted investment and partnerships with European and Chinese suppliers are expanding capacity.

Market dynamics remain volatile. Deliveries and prices fluctuate with public and private infrastructure projects, creating cycles of strong demand followed by sharp declines. Manufacturers and operators must remain flexible to capture opportunities in this irregular procurement environment.

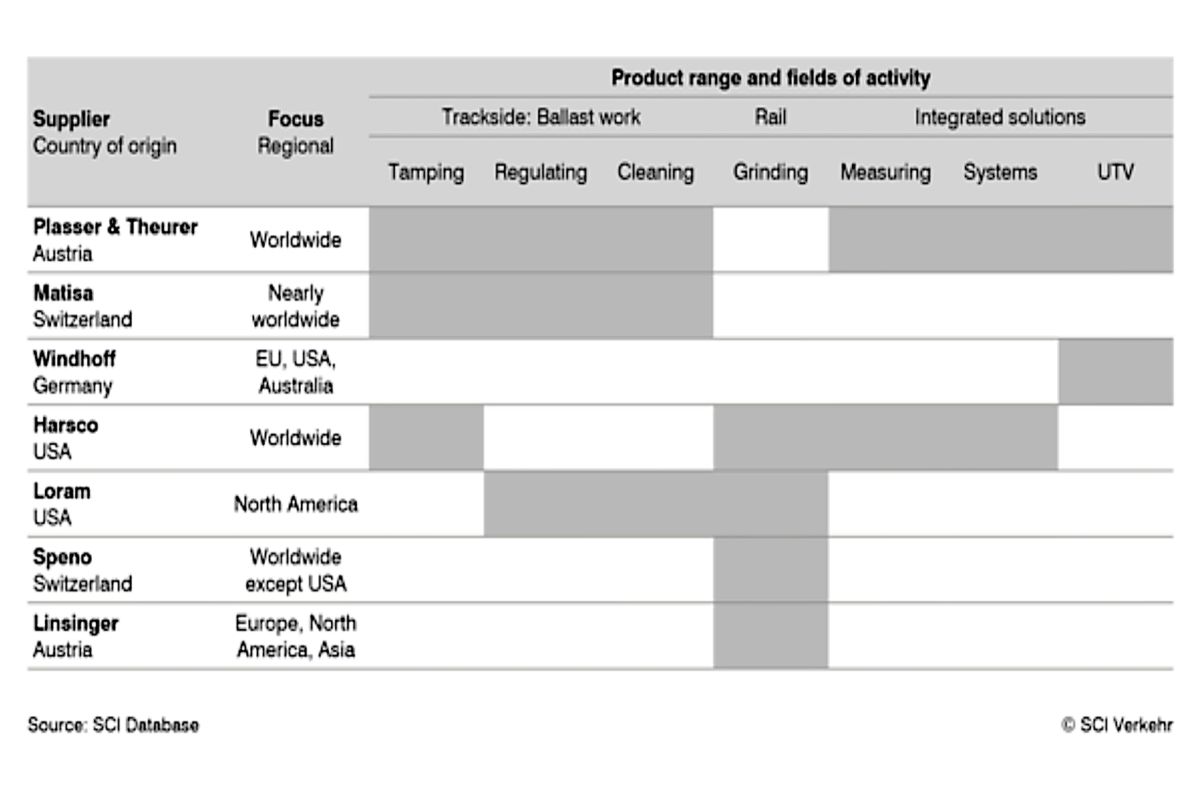

The sector is shaped by a few global and regional specialists. Austria’s Plasser & Theurer leads worldwide, while companies such as Matisa, Windhoff, Harsco and Loram occupy strong regional positions. Increasingly, suppliers are moving toward service-based business models such as full-service contracts, pay-per-use and digital lifecycle management. Hybrid engines, biofuels and battery technology are also entering the market, pushing the ecological standards of the Yellow Fleet higher.

Yellow Fleet at a glance

- Global fleet: ~27,000 vehicles

- Europe: ~7,000 units (largest market, esp. Germany, France, Italy)

- Asia: ~4,900 units (China, India driving growth)

- USA: >4,000 units (mainly freight lines)

- CIS states: large but ageing stock, led by Russia

- Other regions: smaller fleets in Latin America, Africa, Middle East

Leading manufacturers

- Plasser & Theurer (global leader)

- Matisa, Windhoff, Harsco, Loram – key regional roles

Market trends

- Volatile demand cycles tied to infrastructure projects

- Shift towards service-based models (full service, pay-per-use, digital lifecycle)

- Growing use of hybrid, biofuel and battery technologies